4 eyes principle before payment of travel expenses

How can travel expense report controls be automated?

Who checks and how intensively does it have to be?

You may still remember the first two blog posts in this mini-series. Overall, it is about different variants of how travel expenses are to be paid out to travellers. In the first post of the series, we discussed the three basic options: Payment via a SEPA file, payment via payroll or credit-side payment via financial accounting. There are advantages and disadvantages for all variants, whereby we clearly prioritise the last variant.

The second article dealt with the way in which the verification and approval process is organised. In the case of non-digitised processes, 4-eye principles can only be carried out serially. And in times of home offices during Corona, these processes have completely collapsed. Digitisation helps to speed up the processes and to reimburse travellers much sooner.

Feel free to re-read the first two posts.

- The best way to pay travel expenses to business travellers

- Accelerate review and approval processes in travel expense reporting

Today we want to deal with the question of who should actually check what and how extensive this should be. Connected with this is indeed the question, does a human being still have to check at all or under what circumstances can we rely 100% on software here as well? Perhaps this thesis sounds too extreme for you, and at the same time we are experiencing in many areas of life that AI takes care of verification processes for us and we are increasingly relying on it.

What do the supervisors actually check?

In the KickOffs with our clients, we always devote quite a lot of time to the topic of processes around approval and payment, as we see enormous potential for savings and quality improvement here.

Almost always, in addition to the accounting department (We'll look at that below.), the supervisors also check. Usually there is a discussion whether the supervisors should audit before or after the accounting department. In rare cases, our clients also waive the audit by the supervisor.

There is also often a discussion about what should happen if a trip is to be booked to a different cost centre or to a project at the same time. Who controls then? Or there are even more complex conditions that even require multi-level approvals. There was once a case where, for example, within Germany the first management level had to approve, within the EU the next higher level and for transatlantic trips always the management.

Do you know such or similar regulations or discussions? For us, it is absolutely comprehensible where such travel guidelines come from. In the past, with analogous processes, this was to ensure that guidelines were adhered to and costs were kept within limits.

Let's take a realistic look at what supervisors actually check in such cases. Ask yourself:

- Do your superiors know all the legal basics of travel law?

- Do your superiors know all the internal rules of the travel policy?

- Do your superiors know specific limits or similar?

So what do they check? It is conceivable that compliance with budgets is relevant. For this, however, they need evaluations of the travel costs of all travellers of the cost centre or the project. The individual trip does not help here. Or do you check whether this trip was necessary at all? That would also be rather bizarre. For two points may be assumed:

- Trips are usually agreed upon with the managers before the trip or are part of the original

tasks of the travellers themselves.

- No one gets up early and thinks: Where could I go on business today without a reason?

We can therefore assume that the checking and/or approval of travel expense claims by superiors tends to be an annoying additional task or burden for them. At best, an annoying evil perceived as necessary.

Have the courage to ask your managers whether they would be willing to do without it if they were to receive a monthly (or quarterly) evaluation at the same time.

We will outline the possibilities we offer in the last section.

What does the accounting department check?

The second pair of eyes in the four-eyes principle, the accounting department (or sometimes it is also located in the human resources department), is a different matter. Here we can assume the appropriate expertise, although with laws and regulations changing rapidly in some cases, this is not always 100% the case in travel expenses law.

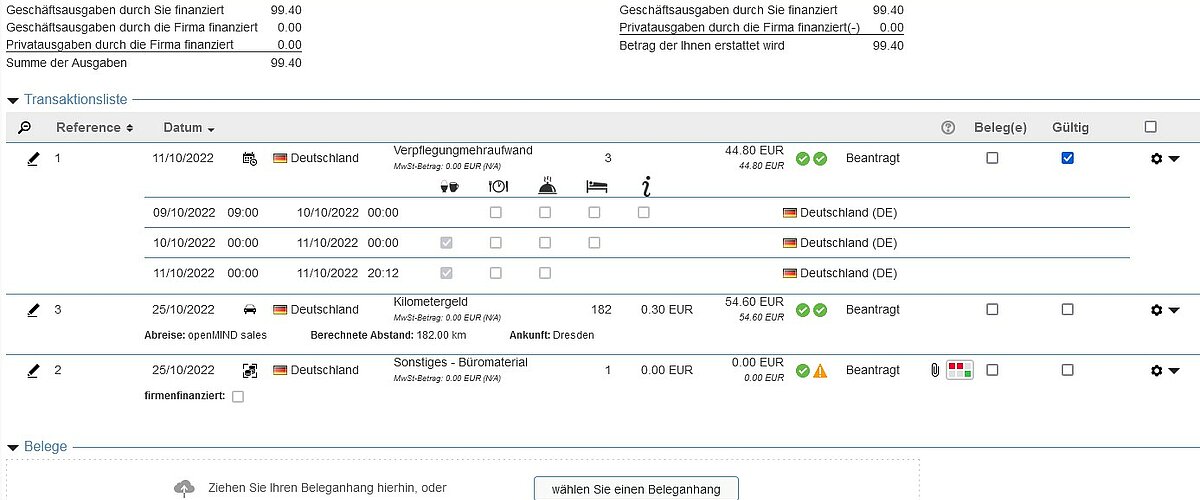

In addition to checking travel expense reports for compliance with laws and travel guidelines, the focus here is certainly on checking receipts.

- Is there a receipt for each transaction?

- Are the receipts correct (e.g. hotel receipt contains company name, taxi receipt also has the correct

VAT ticked etc.)?

- Are receipts correctly split (e.g. in the restaurant drinks; food; tip)?

- Is additional information correct, such as persons served or given gifts?

- Are there any tax aspects arising from the transaction (e.g. is there a flat rate tax or even an

individually taxable portion)?

- Do the settled values agree with the receipts?

- etc.

In the area of additional meal expenses, it is then mostly a matter of aspects such as the following:

- Are the arrival and departure times correct?

- Is the correct country, the correct city selected

- Are corresponding reductions correctly noted

- If necessary, must the 3-month rule be applied?

- etc.

We understand all those in the accounting department who have insisted so far that all receipts and transactions are to be checked here before it is posted to the debit and credit side in the financial accounting department and then paid out. With most of our clients, at least in the first few months of cooperation, it is also organised 100% in this way.

And at the same time, we would also like to discuss this at least once.

What could audit processes look like in the future?

To be able to answer this question, the mandatory steps should be clear. And then, in a second step, we can look at whether and how this can be done reliably by machines or where human intervention is mandatory.

In the following, I would like to outline which possibilities we already have today to carry out the inspection process 100% automatically from our point of view and which steps we also offer to gradually get people used to it, to observe any reservations that may exist and then to reduce them in practice.

What is mandatory?

- A 4-eyes principle in the control

- Monitoring of all legal regulations

- Monitoring of all organisation-specific rules of the travel policy

- Control that all receipts are digitally available

- Control that all essential values are correctly entered in the system

- Cross-checks and plausibility checks

All these points are fulfilled with our solution, which we would like to explain in more detail in the next section.

The 4-eyes principle is fulfilled by independent software systems. In the first step, the values of the receipts are either imported via interface from the credit card providers or read out from the digitised receipts using OCR. It doesn't matter whether the receipt is digitally captured with our APP or simply sent to our system by e-mail. Then, in a second step, the capture is checked by a second software which concentrates completely on whether the values in the system's database match the values on the receipts 100%. If discrepancies are detected, these receipts are visually marked so that inspectors can take a closer look at these receipts and then correct them if necessary.

Legal regulations are always supplied and regularly updated by us. This applies not only to German law, but to over 80 countries worldwide.

However, it is also important to monitor customer-specific rules. Perhaps you have limits for hotels, for flights or you pay different VMAs, etc. Here, it is important for us to discuss each rule in detail with you as specialists and to map it in the system. The system itself then monitors these (and the laws) within the framework of a traffic light system. Documents marked RED can NOT be submitted because laws are disregarded or corresponding rules are broken. Receipts marked GREEN comply 100% with all rules, so do not need to be checked again. This leaves those marked YELLOW. Here there are rule violations for which you may consider an exemption. For these cases, we can digitally enforce a justification to help you make a decision.

In order to be able to destroy paper documents, each document must be digitised and archived in accordance with the GoBD. Our system checks this via the rule that a digital document MUST be attached to each transaction. But what if the travellers attach false PDFs or photos. Then the check reveals that a digital attachment is there. You remember the 4 eyes principle? Of course, the second verification software will sound the alarm and flag this document. It also checks that the values in the database are identical to those on the receipts. This also applies if travellers enter the receipts manually, which is also possible but completely unnecessary.

In addition, there are many cross-checks in the system. Here is a small selection:

- Is the meal reduction marked in the VMA if the person appears on a hospitality receipt at the same time.

- 3-month rule monitoring before payment of the VMA

- Is it actually hospitality or a gratuity

- etc.

We can see that good software systems are already able to carry out 100% of the checks (also in the 4-eyes principle). Errors are already minimised during the recording and before the submission of travel expenses through rules and instructions. People intervene in the few cases where the software has detected errors.

Our experience is that this far-reaching relinquishment of the control function usually does not work at the start of the project. All parties involved must first gain confidence in the functioning of the software and the testing systems. For this reason, there are some ways to gradually move towards automated control.

Managers, for example, can decide for themselves whether they want to check all issues or not. They can decide, logged in the system, that only documents marked YELLOW are displayed to them. This greatly reduces their workload.

Auditors can decide for themselves to only take a closer look at vouchers marked in red according to the 4-eyes principle. Or we can set up rules so that a defined percentage of each document category must be checked. (e.g. 15% of flights; 10% of hotels etc.)

Conclusion

You can see that today, with really well-designed systems using AI, it is almost 100% possible to delegate such routine checks to the machines, thus freeing up valuable working time for specialists and managers to actually do valuable work.

We are convinced that the next few years will see further major advances, particularly in the field of machine learning (AI), so that we will be able to have more and more of these recording and checking processes carried out by software. Please also read our blog posts on AI. LINK

At the same time, our customers are valuable partners for us. This also means that we can, of course, also map the processes that are still established in the majority today with human 4-eye controls. We do not force anyone to use every function of the software. It should serve and benefit people. (not vice versa.)

We would like this contribution to be understood as a proposal for discussion. We would be very happy to enter into direct discussion with you in a meeting or you can also write us feedback.

If you missed the beginning, please also read here:

- The best way to pay travel expenses to business travellers

- Accelerate review and approval processes in travel expense reporting

If you don't want to miss anything, please follow us on LinkedIn or facebook.